Although BILL (currently trading at $49.04 per share) has gained 7.6% over the last six months, it has trailed the S&P 500’s 23.8% return during that period. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Given the relatively weaker price action, is now a good time to buy BILL? Or are investors better off allocating their money elsewhere?

Why Does BILL Spark Debate?

Transforming the messy back-office financial operations that plague small business owners, BILL (NYSE:BILL) provides a cloud-based platform that automates accounts payable, accounts receivable, and expense management for small and midsize businesses.

Two Things to Like:

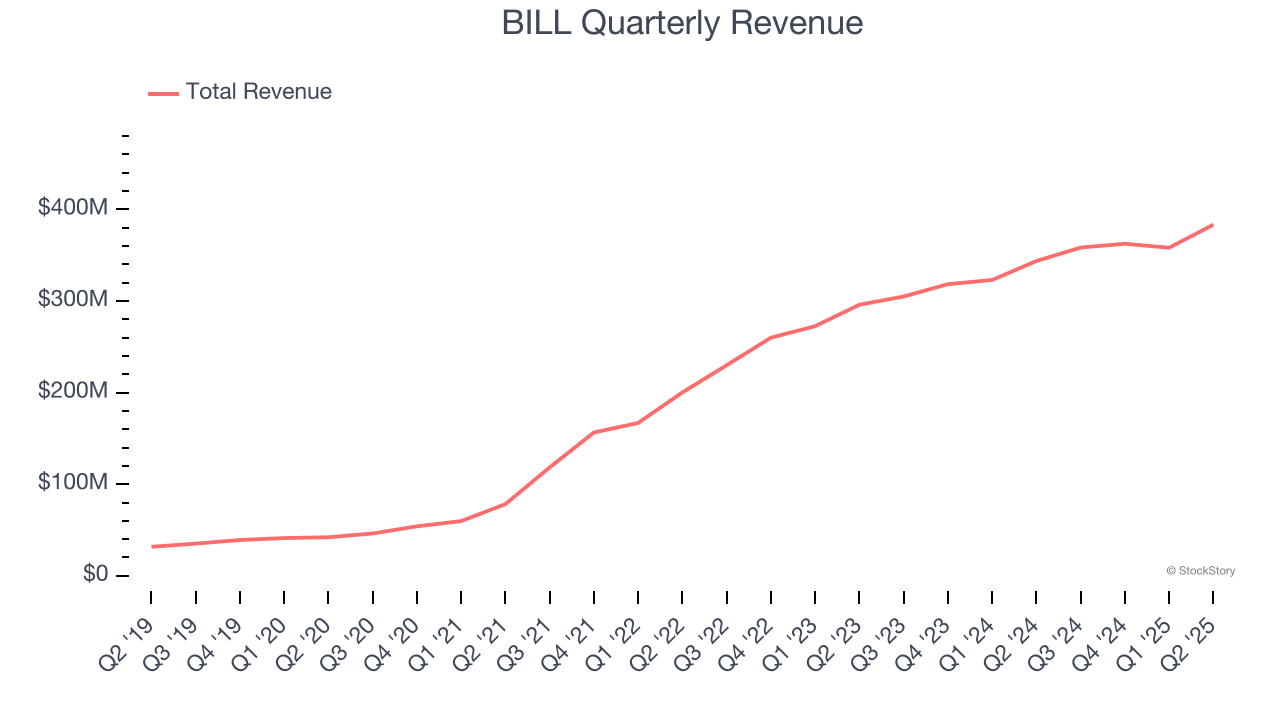

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, BILL’s sales grew at an incredible 56.1% compounded annual growth rate over the last five years. Its growth surpassed the average software company and shows its offerings resonate with customers.

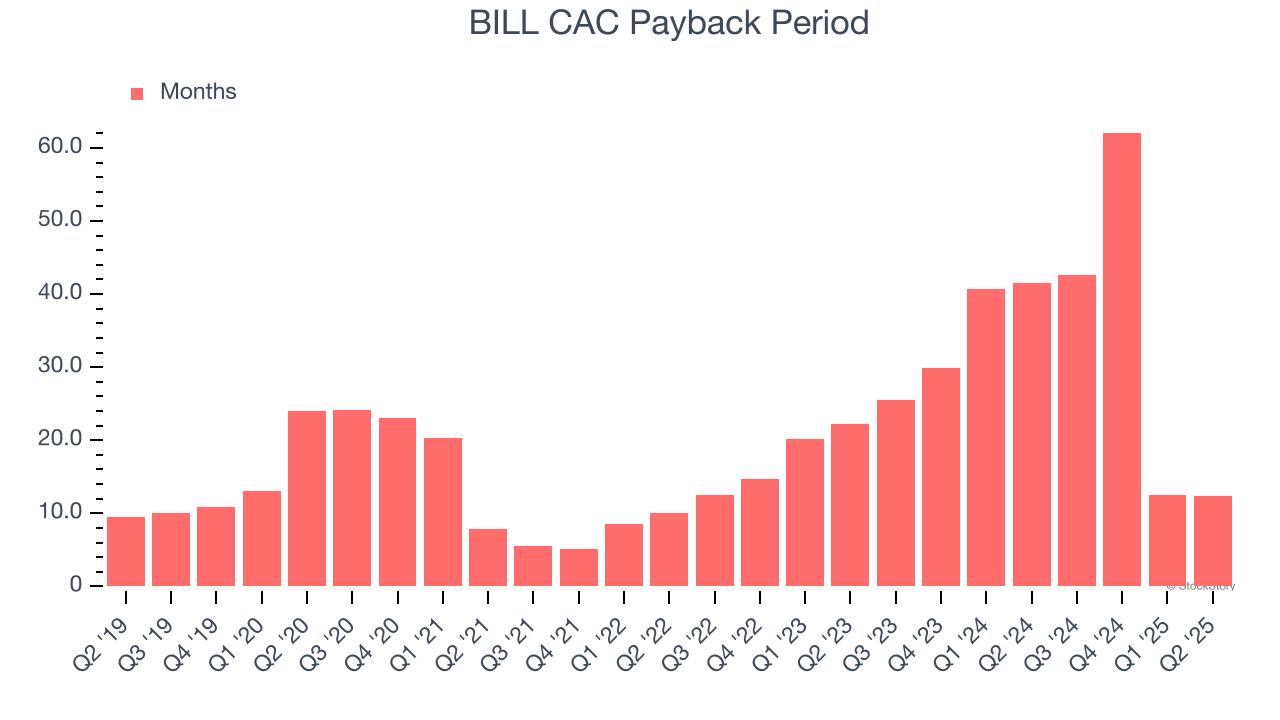

2. Customer Acquisition Costs Are Recovered in Record Time

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

BILL is extremely efficient at acquiring new customers, and its CAC payback period checked in at 12.4 months this quarter. The company’s rapid sales cycles stem from its strong brand reputation and self-serve model, where it can onboard many small customers with little to no oversight. These dynamics give BILL more resources to pursue new product initiatives so it can potentially move up market and serve enterprise clients, which can provide a second leg of growth.

One Reason to be Careful:

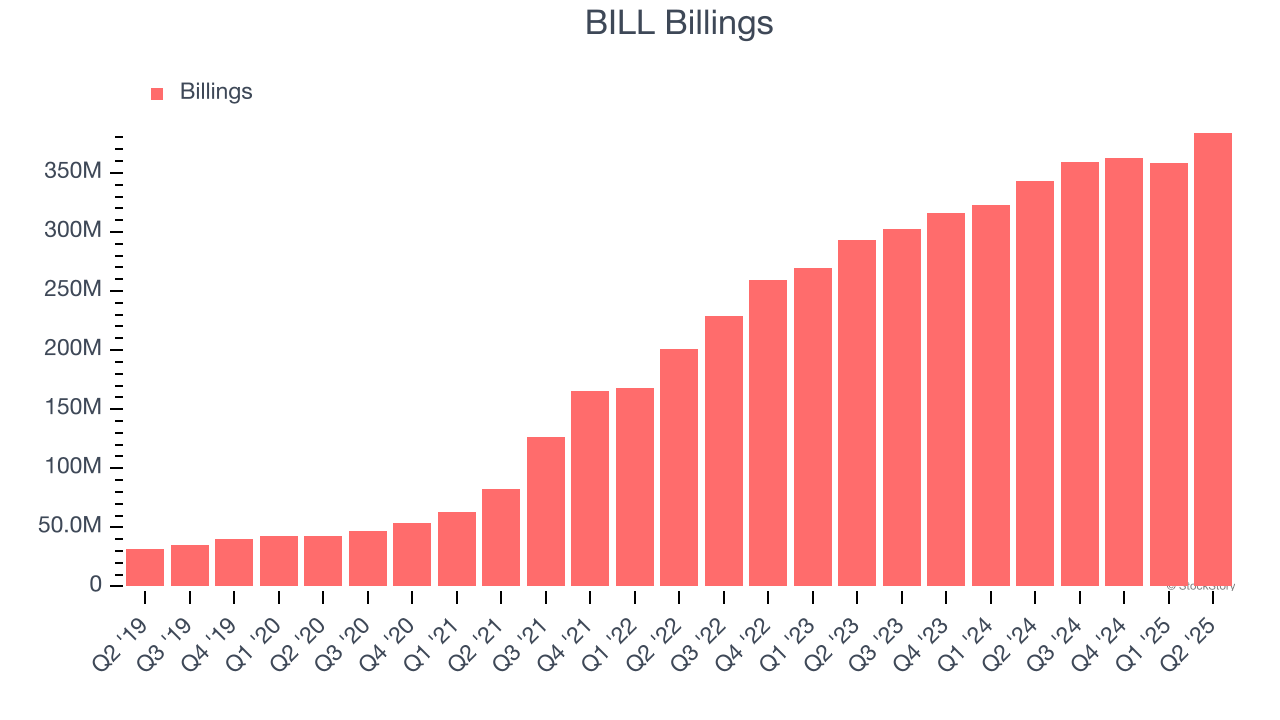

Weak Billings Point to Soft Demand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

BILL’s billings came in at $384.1 million in Q2, and over the last four quarters, its year-on-year growth averaged 14.1%. This performance slightly lagged the sector and suggests that increasing competition is causing challenges in acquiring/retaining customers.

Final Judgment

BILL has huge potential even though it has some open questions. With its shares trailing the market in recent months, the stock trades at 3.1× forward price-to-sales (or $49.04 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free for active Edge members .

Stocks We Like Even More Than BILL

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.